As any Bankruptcy attorney can tell you, the number of people seeking and filing for bankruptcy relief has dramatically declined during the recent pandemic and recovery. In fact, filings are at a 35 year low and dropped nearly 30% from 2019 to 2020 based on overall filings. Enhanced unemployment compensation, mortgage relief and other government programs were all cited as reasons for the historically low filing numbers in the middle of a recession.

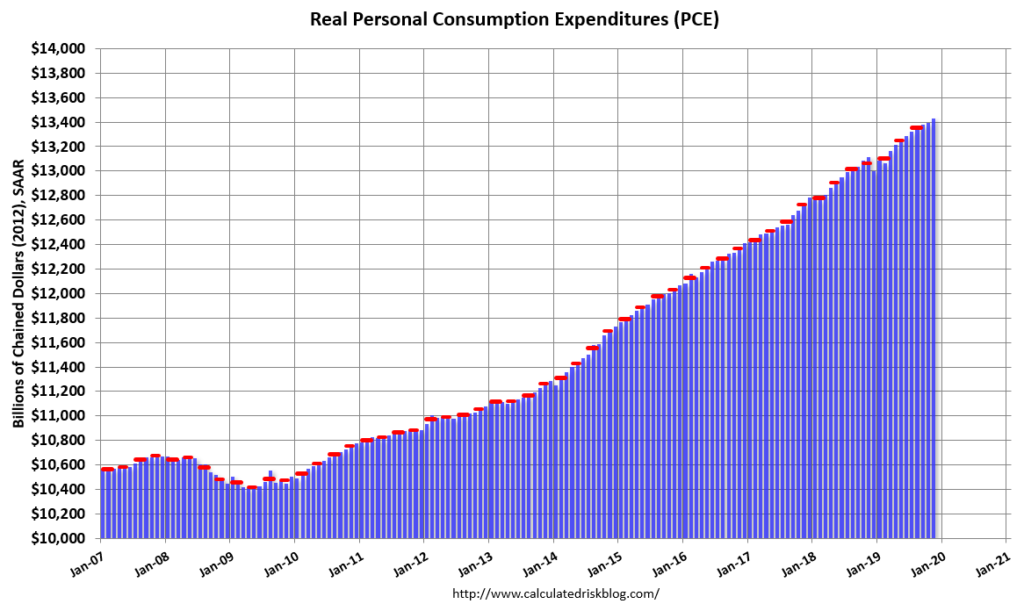

One interesting study was recently published that may help explain the numbers a little further. In April of 2021, credit reporting agency Experian published the following look at consumer debt levels:

https://www.experian.com/blogs/ask-experian/research/consumer-debt-study/

The take away from the article is that consumer debt levels dropped dramatically during 2020. Bankruptcy filings and consumer debt levels have always shared a symbiotic relationship, with each rising and falling in tandem with each other.

Some interesting facts do emerge from the study above. First, not all debt levels decreased equally. First mortgage, car loans and student loan balances all increased. Personal loan levels also increased, but the overall balances’ typical annual growth was cut in half. Credit card debt, second mortgages and other secondary type of loans all declined at approximately 10% from 2019 to 2020. Further examination of the data showed that the lower credit score consumer actually shed the most debt during the 2019-2020 period.

With the above data, it becomes clear that the low bankruptcy filing numbers are a reflection of the ability of consumers to decrease their debt levels in the type of debt that is normally dischargeable in bankruptcy. While mortgage, student loan and vehicle debt increased, those types of debts are typically reaffirmed or maintained through a bankruptcy liquidation. In contrast, retail cards, credit cards, personal loans and even secondary mortgages can all be liquidated in a bankruptcy filing. However, the average consumer was able to reduce the levels on all of the dischargeable type of debt during the 2019 – 2020 time period and was not forced to seek the protection offered by a bankruptcy filing.

For 2021, consumers can expect to see rising mortgage, vehicle and student loan expenses. It remains to be seen if inflation will cause credit card, second mortgage and personal loan balances to increase and cause a bump up in the bankruptcy filing levels later in 2021.

Be sure to obtain the proper legal advice for your financial situation prior to any decision to file bankruptcy. At Mickler & Mickler we fight every day to protect your family from poor financial planning. Our office has the experience and the dedication that you deserve when your family is looking for financial help. Please contact us at 904-725-0822 or bkmickler@planlaw.com for any additional questions.